Talk of a ‘coal comeback’ in the wake of the blockade of the Persian Gulf are disproven by data showing coal generation is down globally.

EUobserver voice is a daily opinion piece by EUobserver staff writers, published every weekday morning.

There have been a string of announcements and reports of late that suggest the world is returning to coal in the wake of the closure of the Strait of Hormuz.

The disruption was described in one media as ‘gravy’ to the world’s dirtiest fuel, and it’s easy to understand why.

About a fifth of global oil and liquid gas passes through the strait, and with the US now blockading a waterlane that was already blockaded, the crisis looks far from over.

And Iran has knocked out almost a fifth of Qatar’s liquid gas production, which ensures gas supply disruptions are here to stay.

Asian countries are most exposed. South Korea, the Philippines, Bangladesh and Pakistan have all announced plans for the extension or expansion of coal generation.

European governments are doing the same. Italy has delayed its coal phase-out by 13 years, while Germany has floated restarting idled coal plants.

Even in the Netherlands, where the coal exit is all but finalised, politicians have discussed extending the lifetimes of the country’s last plants, despite the coal operator saying it may shut them down earlier than planned due to unprofitability.

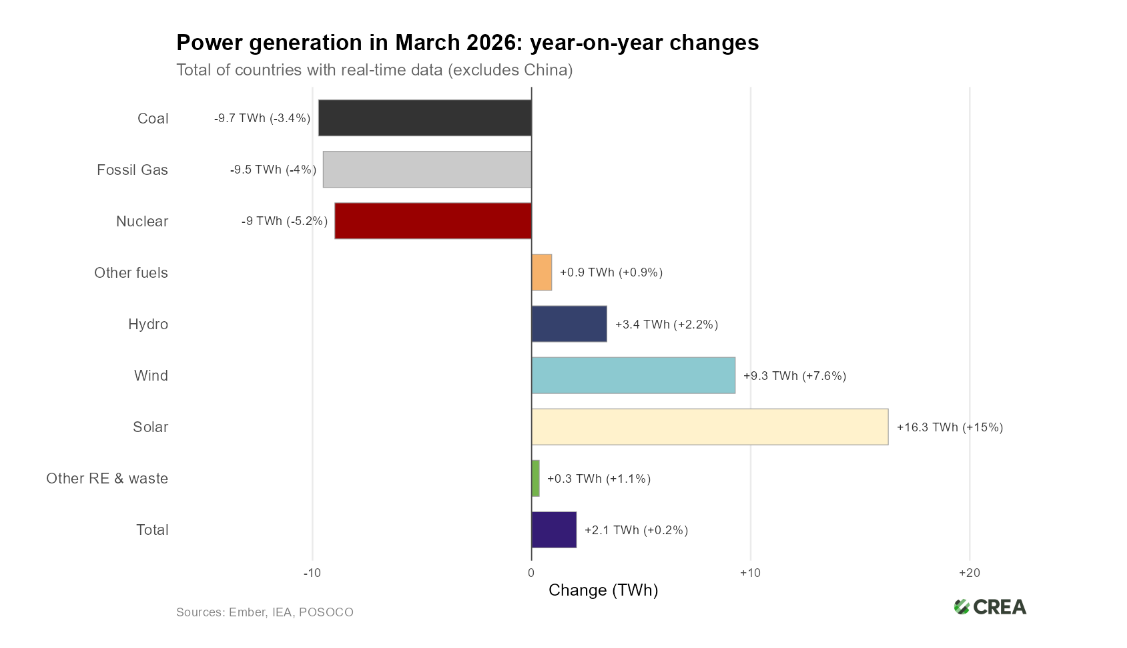

But for all the talk of a “coal comeback”, the data suggests actual coal use is down globally since the start of the war.

Energy think-tank Crea published data on Tuesday (14 April) showing global coal burning is down 3.5 percent in March compared to the same period last year, covering 87 percent of global coal power generation.

“The data contradicts widespread expectations that coal power generation would rise in response to the crisis,” the report notes.

The data does not include China which doesn’t publish real-time power data and where power generation from coal rose two percent according to its own data.

But in all other major coal consuming economies including the US, India, EU, Turkey and South Africa, coal-fired power generation fell.

Gas consumption for power was also down four percent, which can be easily explained by rising prices due to the supply disruption in the gulf of Persia.

Before the war, roughly one-fifth of global liquid gas supply, about 112bn m³, passed through the strait. If used for power, that equals around 590 Terrawatt-hours, roughly France’s annual electricity generation.

This however is more than made up for by renewable additions.

In 2025 alone, data from energy think-tank Ember shows the world added enough new wind and solar capacity to generate about 1100TWh a year, nearly twice as much, which helped reduce the need for more coal since the start of the crisis.

One reason there hasn’t been a coal resurgence is that coal was already cheaper than gas, even before the latest price shock, meaning coal plants are already running close to full capacity.

The only way for coal to “come back is to build new plants, or revive old ones,” Ember’s Dave Jones told EUobserver. And by those metrics, there’s just not that much room to play with.

Germany has seven gigawatt of coal power capacity in reserve. Italy’s total coal generation was under five gigawatts in 2025 — less than one percent of national electricity output, according to the country’s grid operator Terna.

Even if these plants, which currently operate at an €80m a year loss, are extended, it will not materially change either country’s energy outlook. The speed with which renewables can be connected to the grid is the determining factor.

Data from another recent Ember study shows that almost 700GW of renewable projects are waiting for grid connection across Europe.

In Italy alone, 231 GW of projects have a connection agreement but remain unbuilt — nearly twice the country’s entire power capacity.

Building wires sometimes takes decades. But the International Energy Agency estimated that software and contract reforms alone could unlock up to 185 GW of capacity across Europe.

The most important bottleneck, it turns out, isn’t fuel, but the grid.